A Section 754 election can be a favorable tax efficiency tool that is unique to partnerships (as compared to corporations). However, the complexity, administrative burden and changing economic environment should always be considered carefully. Every general partner of a partnership should be aware of these rules and their implications.

Background

The Subchapter of the Internal Revenue Code (“IRC”) that governs the taxation of partnerships, subchapter K, is one of the more complex areas of the code. In general, the taxation of partnerships is a mix between two concepts:

- Entity Method: Treating the partnership as an entity separate and distinct from its owners.

- Aggregate Method: Treating the partnership as an aggregation of its owners, each of whom owns a share of the various partnership assets.

These two differing approaches are highlighted by the concept of “inside” and “outside” tax basis with respect to partners of a partnership.

- Inside Basis: This is a product of the aggregate method. Each partner has proportionate share of the tax basis of the assets in the partnership.

- Outside Basis: This is a product of the entity method. Each partner has a tax basis in his investment in the partnership that is separate and distinct from the assets of the partnership. This is dictated by the items that affect each partner’s basis (contributions, distributions, transfers, allocable items of income and expense items, etc.).

Certain transactions or events during the life of a partnership can result in divergence between the inside and outside basis, and this can result in incongruent tax treatment. At a high level, the purpose of the Section 754 election is to align inside and outside basis to avoid these scenarios. This is done by adjusting the partnership’s basis in those assets (inside basis) to align with the partners’ basis in the partnership (outside basis).

Situations Where a Basis Adjustment Can Be Made

There are two Sections in Subchapter K that allow for basis adjustment if a Section 754 election is in place when the inside and outside basis differ.

Section 743 – Transfer of an interest in a partnership by sale or exchange or on death of a partner.

The transferee partner gets an outside tax basis in the partnership equal to the purchase price of the partnership interest (or fair market value (FMV) of the partnership interest if the result of death of a partner). With respect to inside basis in partnership assets, the transferee partner “steps into the shoes” of the transferor partner and is allocated his proportionate share of basis in the partnership assets. A Section 743 basis adjustment is made to the partnership’s basis in the assets so that the transferee partner’s inside basis is equal to his outside basis. Please note that this adjustment to basis of the assets is only allocated to the transferee partner.

Section 734 – Distribution of partnership assets to a partner.

The distributee partner receives property in exchange for liquidating his partnership interest and recognizes gain or loss on the liquidation of that interest. The amount of gain or loss is based on his outside basis in the partnership, which differs from his proportionate share of the inside basis on the assets that were distributed to him. The basis of the remaining partnership assets can be adjusted by the gain or loss recognized by the distributee partner. This adjustment is allocated to all of the remaining partners.

Basis Divergence Impact

Differing inside and outside basis can have significant impacts on the timing and character of gains and losses recognized by the partners. To illustrate this, see the example below.

This example refers to a Section 743(b) adjustment. These adjustments are more common with hedge funds and private equity funds.

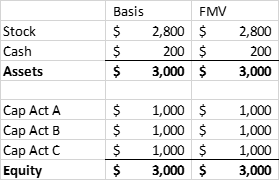

Investment Partnership ABC is formed by partners A, B, and C, contributing $1 million each. ABC purchases a portfolio of stocks and retains some cash to pay expenses. Below is the balance sheet immediately after the formation:

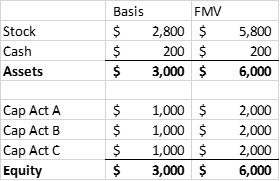

After a period of time, the portfolio of stocks increase in value. However, Partner A decides to sell his investment to Partner D, equal to the FMV of his capital account.

BEFORE SALE OF INTEREST

AFTER SALE OF INTEREST

Partner D has an outside basis equal to the purchase price of $2 million. However, his allocable share of the partnership’s inside basis in the stock is $1 million (1/3 of $3 million). Partner A realized a $1 million gain from the sale of his partnership interest, which was the result of the unrealized appreciation of the stock portfolio. If Partnership ABC subsequently decides to then sell its portfolio of stocks, it would realize a gain of $3 million, which would then be allocated to the remaining partners (including Partner D).

The effect is that both Partner A and Partner D were taxed on the same gain, which is obviously not an optimal outcome.

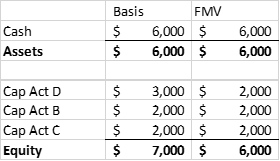

If in a later tax year the partnership decided to liquidate, Partner D would realize a tax loss of $1 million (as the result of a higher tax basis). This would seem to correct the earlier double tax situation. However, there is the issue of the timing as well as the limitation on the deductibility of a capital loss. If Partner D is an individual who does not have capital gains to offset the capital loss in the year of liquidation, he is limited to a deduction of $3,000. This could result in a double tax situation that may take a significant amount of time to correct.

How the Adjustment Works

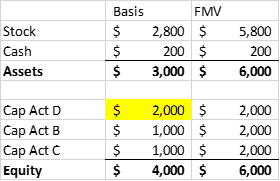

The above scenario can be remedied by the fund making a Section 754 election and adjusting the basis pursuant to Section 743(b). The adjustment in the basis of the assets of the partnership is equal to the transferee partner’s initial basis in the partnership less his proportionate share of the adjusted basis of the partnership assets. In the example above, the basis in the partnership assets would be stepped up by $1 million ($3 million initial outside basis less $2 million of adjusted inside basis in the assets).

Again, it’s important to remember that with IRC Section 743(b), the entire basis step up is allocated to the transferee partners.

Allocation of Basis Adjustment

The regulations under IRC Section 755 provide guidance regarding how to allocate the basis adjustment. There are three scenarios described in the regulations:

- Section 743(b) adjustment with non-substitute basis (i.e. sale or exchange or transfer by death)

- Section 743(b) with substitute basis (i.e. nontaxable transfer)

- Section 734(b) transaction

For purposes of this post, we will focus on the Section 743(b) transfer with non-substitute basis as that is the most applicable to hedge funds and private equity funds.

FMV is assigned to all partnership assets, and all assets must be classified as either capital assets/Section 1231 property (capital gain property) or other property (ordinary income property). In a fund context, the vast majority of assets would likely be capital gain property. First, the basis adjustment is allocated among the two classes and then allocated to each asset within the class.

The allocation of the basis adjustment between the classes and within each class is dictated by allocation of gain or loss that the transferee partner would receive if, immediately after the transfer of partnership interest, the partnership had a hypothetical liquidation to the FMV of the assets. The basis for determining the “hypothetical” gain or loss is the carryover tax basis of the transferor partner.

- The amount allocated to the ordinary class would be the total income, gain, or loss that would be allocated to the transferee partner from the sale of ORDINARY property

- The remainder would be allocated to capital property

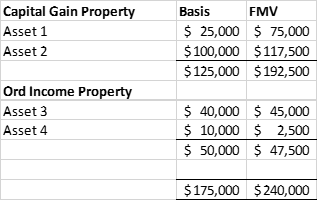

EXAMPLE [Treas. Reg 1.755-1(b)(2)(ii) example 1]

- Partner A contributes $50,000 cash and Asset 1 (below) with FMV of $50,000 and tax basis of $25,000 (giving him tax basis of $75,000).

- Partner B contributes $100,000 cash.

- After the asset value increases to $240,000, Partner A sells his interest to Partner T for $120,000 (FMV). See Balance Sheet below.

- A hypothetical liquidation would give Partner T a net realized gain of $45,000 (proceeds of $120,000 less Partner A’s carryover basis of $75,000).

- The ordinary portion of the gain/loss would be a loss of $(1,250) (50% of the FMV of $47,500 less basis of $50,000). That leaves $46,250 of gain to be allocated to capital gain property.

- Between the assets in each group, the allocations of the basis adjustment are in accordance with T’s gain or loss that would result in the hypothetical sale of each asset. See below.

Mandatory Basis Reduction

As you can see from the above example, the election to “step up” the partnership’s basis in its assets is a taxpayer friendly election. Unfortunately, when a situation arises where a partner’s outside basis is less than his respective inside basis, a partnership may be required to “step down” the basis. In the example above, we saw how, absent a basis “step up,” a double tax situation could result. Similarly, when outside basis is less than inside basis, a situation could arise where two taxpayers take the same deduction.

Both Section 743 and 734 were amended by the 2004 Jobs Act to include a mandatory basis reduction if a partnership has a “substantial built-in loss” immediately after a transfer of interest (Section 743) or a partnership has a “substantial basis reduction” immediately after the distribution of partnership assets (Section 734).

Substantial Built-in Loss (Section 743): The total of the partnership’s tax basis in its assets exceeds the total Fair Market Value of its assets by more than $250,000 immediately after the transfer of interest. Again, this is only allocated to the transferee partner.

Substantial Basis Reduction (Section 734): The distribution of property results in the distributee partner receiving a property with an inside basis less than his outside basis, and the distributee partner recognizes a loss of greater than $250,000. This loss is allocated to all remaining partners.

Other Issues

There are a few other items that should be taken into consideration before a fund makes an IRC Section 754 election. First, it is irrevocable without consent from the IRS. Once the election is in place, any transaction that meets the definition of Section 743 or 734 will require a basis adjustment, whether it is tax favorable or tax unfavorable. In the hedge/private equity space, a Section 754 election could be made in a time when the fund is in a net appreciated position, but the markets could change and the fund could find itself in a net depreciated position when Section 743 or 734 transactions occur. This is something that should be taken into account.

Additionally, because the adjustment is made on an asset by asset basis, and because there could be multiple Section 743 or 734 transactions, it is possible that the tracking of the adjustment could become administratively burdensome. This should be factored in as well.

In Conclusion

A Section 754 election can be a favorable tax efficiency tool that is unique to partnerships (as compared to corporations). However, the complexity, administrative burden and changing economic environment should always be considered carefully.

Furthermore, the mandatory basis reduction should always be considered as this can prove to be a trap for the unwary. Every general partner of a partnership should be aware of these rules and their implications.