On August 23, 2018, the PCAOB provided supplemental information to PCAOB Release No. 2017-001, The Auditor's Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion and Related Amendments to PCAOB Standards.

This guidance was originally published on June 1, 2017 in conjunction with the adoption of PCAOB Auditing Standard AS 3101. Release 2017-001 and AS 3101 require changes to the auditor’s report in an effort to:

- Clarify the auditor’s role and responsibilities related to the audit of the financial statements

- Provide additional information about the auditor

- Make the auditor's report easier to read

The August 2018 updates appear to further the PCAOB’s original intent of Release No. 2017-001. They offer additional guidance in making the auditor’s report easier to read and more useful to stakeholders, while still maintaining the pass/fail opinion model for audit reports. Specifically, the updates focus on:

- Providing aid to the auditor in applying the concepts in the original release, such as determining auditor tenure

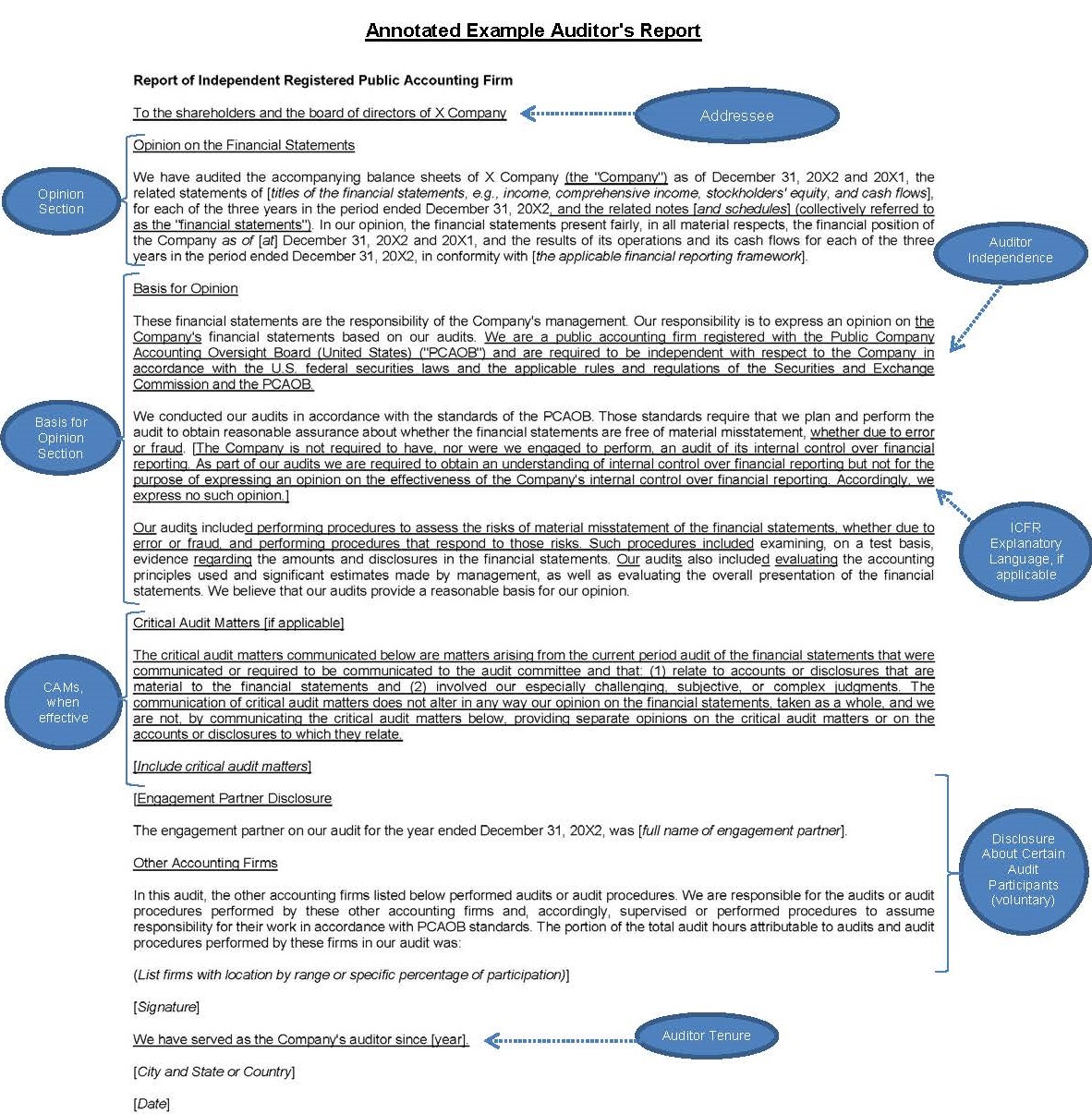

- Further standardizing the reporting model by specifying placement and providing examples of disclosures and providing guidance in situations where auditors decide to include voluntary disclosures of information currently required to be disclosed in Form AP, Auditor Reporting of Certain Audit Participants.

The updates relevant to audit reports on investment companies registered with the SEC are summarized below:

Voluntary Disclosure About Certain Audit Participants

PCAOB Form AP, Auditor Reporting of Certain Audit Participants, requires reporting of certain information regarding the engagement partner and other accounting firms participating in an audit. Auditing standards permit, but do not require, the audit firm to include in the report information about the engagement partner and/or other participants in the audit. If the audit firm chooses to disclose this information, there are requirements:

- The engagement partner’s name must be presented in full, consistent with Form AP

- If the auditor includes information about the other audit firms in the auditor's report, all other accounting firms required to be disclosed on Form AP must also be included in an appropriately titled section of the report (example below) with the following information:

- A statement that the auditor is responsible for the audits or audit procedures performed by the other public accounting firms and has supervised or performed procedures to assume responsibility for their work in accordance with PCAOB standards

- Other audit firms individually contributing 5% or more of total audit hours are required to disclose information consistent with that required by Form AP, including:

- Firm's legal name

- Firm’s city and state (or, if outside the United States, city and country) of the headquarters' office

- Percentage of total audit hours as a single number or within an appropriate range

- Other audit firms individually contributing less than 5% of total audit hours are required to disclose information consistent with that required by Form AP, including:

- The number of other audit firms individually representing less than 5% of total audit hours

- The aggregate percentage of total audit hours of such firms as a single number or within an appropriate range

Uncertainty About the Specific Year For Tenure

If there is uncertainty of the tenure of the audit firm, the auditor should state as much in its report and provide the earliest year which the auditor has knowledge it served as auditor. An illustration of that language is also provided.

The update also states that it is not acceptable for an audit firm to make a statement or imply that the auditor did not determine its tenure.

The update also addresses scenarios when an auditor's report is reissued by a predecessor auditor and states that the predecessor auditor may expand the tenure statement to indicate when its tenure ended.

Examples of various specific scenarios are also provided to aid an auditor in determining the date of tenure.

Guidance Added For Reporting Auditor Tenure in Separate Report on Internal Control Over Financial Reporting

Registered investment companies are not required to have auditors opine on their assessment of the company’s internal control over financial reporting, but the auditor does issue a separate report on any internal control findings as a result of its audit of the financial statements. These findings are disclosed in the auditor’s report on the financial statements. This update specifies the location for the reference to the auditor’s report on the internal control and also notes that the auditor’s tenure is not required to be disclosed in the separate internal control report.

Further Guidance on Placement of Explanatory Paragraphs

The update recognizes that there are certain explanatory paragraphs such as going concern considerations, material changes in accounting principles and corrections of material misstatements that are required to be presented with an appropriate title immediately following the opinion paragraph. However, to the extent that an explanatory or emphasis paragraph is needed pertaining to other considerations, there is no guidance on placement, and the auditor should use its judgement in placement and appropriately title the section.

Examples of emphasis paragraphs include:

- Significant transactions, including significant transactions with related parties

- Unusually important subsequent events, such as a catastrophe that has had, or continues to have, a significant effect on the company's financial position

- Accounting matters, other than those involving a change or changes in accounting principles, affecting the comparability of the financial statements with those of the preceding period

- An uncertainty relating to the future outcome of significant litigation or regulatory actions

- That the entity is a component of a larger business enterprise.

The update includes an appendix with information for reporting on Special Situations, including:

- Supplemental information – The updates recognize that since there is no requirement in terms of specific location, the auditor should use its judgement for placement and title appropriately to aid the reader in distinguishing the auditor's report on supplemental information from the other sections of the auditor’s report on the financial statements

- Review of Interim Financial Information - Provides an example of how to meet the disclosure requirements relating to a review of interim financial information and specifically the auditor’s independence

- Special Reports – The update specifically references AS 3305, Special Reports, which provides reporting requirements for various types of special reports, such as reports on specified elements, accounts, or items of a financial statement

An annotated example auditor's report from the PCAOB's Staff Guidance on Changes to the Auditor's Report, updated on August 23, 2018, appears below. The full Staff Guidance document from the PCAOB can be found here.