This post is the first in a three-part series that examines implications of the 2017 Tax Cuts and Jobs Act for the investment management industry. Part Two will detail the effect of Section 199A on financial products and investors. Lastly, Part Three will examine the deduction and C Corporation to S Corporation transitions. Feel free to be in touch with Matt Romano, tax partner, with questions about how these complex new tax developments affect you and your business.

OVERVIEW

Included in the 2017 Tax Cuts and Jobs Act was a new deduction for business income from pass-through entities (“PTE”) and sole proprietorships. This deduction (Section 199A) will provide a deduction up to 20% of a taxpayer’s qualified business income (“QBI”) from a PTE. Absent the limitations that are discussed later in this post, this deduction would operate to limit the top tax rate to 29.6% for business income from a PTE (80% of the top individual rate of 37%).

The deduction is not a component of adjusted gross income (“AGI”). Rather, it is a deduction from AGI to arrive at taxable income (e.g. no effect on limitations based on AGI). The deduction is available whether or not the taxpayer itemizes or uses the standard deduction.

QUALIFIED BUSINESS INCOME

According to the Internal Revenue Service, QBI for a given year is the “net domestic taxable income, gain, deduction, or loss with respect to any qualified trade or business” of the taxpayer. Amounts are included to the extent they are included in the determination of taxable income for that year. This would typically be Box 1 on a taxpayer’s Schedule K-1. However, separately stated items that are used to calculate taxable income are also included (e.g. Section 179 deduction, Section 1231 gain/loss, etc.)

Exclusions include:

- Investment income (e.g. interest, dividends, short & long term capital gains)

- The QBI deduction is strictly for domestic taxable income. If there is a mix of foreign and US- based income, proration will need to be used. Foreign items excluded include commodities gains, foreign currency gains, or other similar items.

- Partner payments, paid in compensation for services, guaranteed payments for partnerships/LLCs, as well as other ‘disguised’ payments for services

- S-Corp “reasonable compensation”

Business Structures Where Section 199A Applies:

QBI would apply to the following businesses structured as relevant pass-through entities (RPEs):

- Sole proprietorships (no entity, Schedule C)

- Real estate investors (no entity, Schedule C)

- Disregarded entities (single member LLCs)

- Multi-member LLCs (not including C Corp electing ones)

- Any entity taxed as a partnership, filing Form 1065

- Any entity taxed as an S-Corp, filing Form 1120-S

- Trusts & estates, REITs and qualified cooperatives

How does the QBI deduction work in general?

A QBI deduction cannot exceed the lesser of:

- Combined QBI from all RPE x 20%

-or-

- Taxable income minus capital gains x 20%

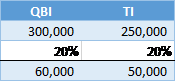

Example:

- Consider the case of a married teacher

- With QBI income of $300,000

- Married filing jointly (MFJ) taxable income of $250,000

What is the QBI deduction in this scenario? [$50,000]

Specified Service Businesses: Where Section 199A Meets the Investment Management Industry

Specified Service Business, (SSTB): Section 1202(e)(3)(A) of the IRC defines an SSTB as “any trade or business involving the performance of services in the fields of health, law, accounting, actuarial sciences, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees or owners.”

Proposed regulations originally narrowly defined “skill or reputation” to celebrity appearances, endorsements, or similar considerations.

However, this definition was further expanded to include “services that consist of investing and investment management, trading, or dealing in securities, partnership interest or commodities, as defined in section 475(e)(2).”

Specified Service Limitation

If the PTE is determined to be a Specified Service Business, then the deduction may be subject to limitation based on the taxpayer’s taxable income. Please see the chart below.

This specified service limitation does apply to Investment Managers, Advisors, or Dealers in Securities (See IRC Section 199A(d)(2)(B)).

Taxable Income Considerations

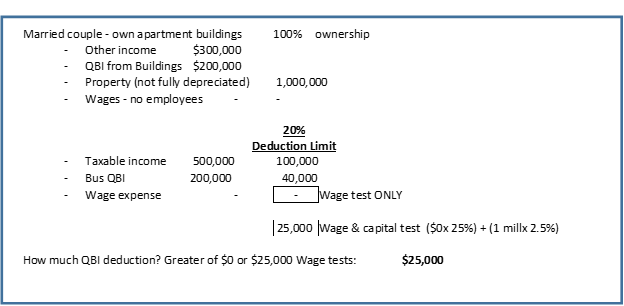

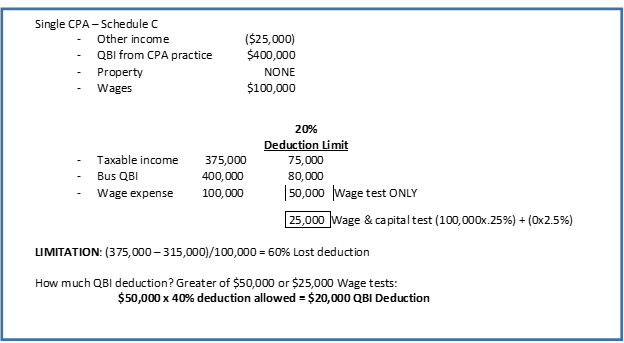

Non-Specified Service Businesses- Wage & Cap Testing

For PTEs that are NOT Specified Service Businesses, the taxpayer would need to consider the W-2 Wage limitation. If the taxpayer’s taxable income exceeds $207,500 (single) or $415,000 (MFJ), then the 20% QBI deduction would be limited to the greater of the following:

- 50% of the taxpayer’s allocable share of W-2 wages paid by the PTE during that year. W-2 wages are generally the sum of wages paid subject to withholding, elective deferrals, and deferred compensation.

-or-

- 25% of the taxpayer’s allocable share of W-2 wages PLUS 2.5% of the “unadjusted basis” (typically cost basis) of all qualified property.

- Qualified property is tangible property that is subject to depreciation that is held by, and available for use in a “qualified trade or business” and used in the production of QBI, for which the depreciable period has not ended before the close of the taxable year.

- Unadjusted basis: Equal to basis immediately after acquisition

Non-Specified Service Example

Specified Service Example

MULTIPLE QUALIFIED BUSINESSES

Aggregating businesses can allow a taxpayer facing wage and property limitations to claim a higher QBI deduction by aggregating a business subject to the limitations with a business that has more wages and/or property to allow deduction. Under the proposed regulations, however, there are requirements that must be met to aggregate multiple PTEs.

QBI LOSSES

If an individual's QBI from at least one trade or business is less than zero, the individual must offset the QBI attributable to each trade or business that produced net positive QBI with the QBI from each trade or business that produced net negative QBI in proportion to the relative amounts of net QBI in the trades or businesses with positive QBI.

If the Net amount of qualified income, gain, deduction and loss with respect to qualified trades or businesses of the taxpayer for any taxable year is less than zero, such amount will be treated as a loss from a qualified trade or business in the succeeding taxable year (e.g. carried forward).

This carryover rule does not affect the deductibility of the loss for purposes of other provisions of the Code. The W-2 wages and UBIA of qualified property from the trades or businesses which produced net negative QBI are not taken into account for this purposes, and are not carried over to the subsequent year.

Example:

2018 Total loss of ($180,000), therefore, 2018 QBI is $0 → no deduction taken

2019 Total profit of $250,000, 2019 QBI is $70,000 ($250,000 – $180,000). The 2019 199A deduction will be based on reduced income of $70,000, not the full $250,000.

CONCLUSION

While the new tax regulations were intended to simplify the tax code, there is a complexity to the determination of the QBI deduction due to the various rules and requirements. It may seem as though you might not be able to benefit from this deduction due to the income thresholds. However, there are tax planning opportunities that can result in your ability to take advantage of the additional savings.

**Final regulations have not yet been released and changes may be made to the above proposed regulations.